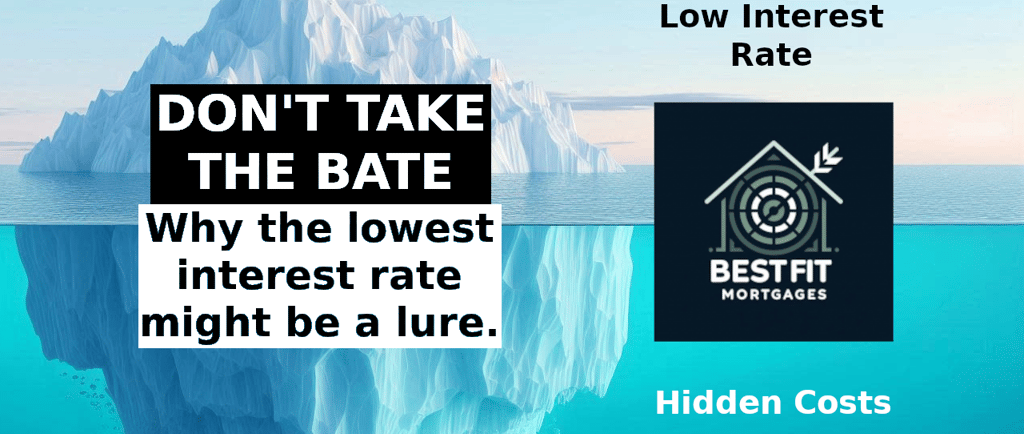

Tip of the Iceberg: Navigating the Hidden Depths of Mortgage Costs

When you're in the market for a mortgage, it's easy to get caught up in the interest rate game. After all, a lower rate means lower monthly payments, right? While that's true, at Best Fit Mortgages LTD, we're here to tell you that there's more to the story. Let's dive into why the mortgage with the lowest interest rate isn't always the best deal in the long run.

Best Fit Mortgages LTD

9/13/20242 min read

The Allure of Low Interest Rates

It's no secret that low interest rates are attractive. They catch your eye in advertisements and can make a mortgage seem like a great deal at first glance. However, savvy homebuyers know that the interest rate is just one piece of the puzzle.

Unveiling the Hidden Costs: Bank Fees

When you're comparing mortgages, it's crucial to look at the fine print. Banks often charge a variety of fees that can significantly impact the overall cost of your mortgage. These may include:

Application fees

Valuation fees

Arrangement fees

Early repayment charges

Sometimes, a mortgage with a slightly higher interest rate but lower fees can actually be cheaper over the fixed term period. This is especially true for less expensive mortgages, where fees make up a larger proportion of the overall cost.

The Cashback Conundrum

Some mortgage products come with cashback offers, which can be very appealing. These offers provide you with a lump sum when you take out the mortgage, which can be helpful for covering moving costs or other expenses.

However, it's important to weigh the cashback amount against any higher interest rates or fees. In some cases, a mortgage with cashback and a slightly higher rate could work out cheaper overall than a low-rate mortgage without cashback.

Understanding Total Cost

To truly compare mortgage offers, you need to consider the total cost over the fixed period. This is where the real comparison happens, and it's more complex than just looking at the interest rate. Here's what you need to consider:

Total interest paid: This is a significant factor. Even small differences in interest rates can have a substantial impact over time.

All fees and charges: Add up every fee associated with the mortgage.

Cashback or incentives: Consider any financial incentives offered.

By looking at these factors together, you get a more accurate picture of the mortgage's true cost. Sometimes, a mortgage with a slightly higher interest rate might actually be cheaper overall when you factor in lower fees or generous cashback offers.

Conclusion: Make an Informed Decision

While a low interest rate is certainly a factor to consider, it shouldn't be the only one. By taking into account the total interest paid, fees, cashback offers, and calculating the total cost over your fixed term, you can make a more informed decision about which mortgage truly offers the best value.

Remember, the right mortgage isn't just about today's payments – it's about finding a financial solution that works for you in the long term. At Best Fit Mortgages LTD, we're here to help you navigate these waters and find the mortgage that truly is the best fit for you.

Want to know more about how to find the right mortgage for your situation? Contact Us today for personalized advice and guidance. We can help you analyze all aspects of potential mortgages and find the one that will save you the most in the long run.

BEST FIT MORTGAGES LTD

T: 01744411604

E: contact@bestfitmortgages.co.uk

Your property may be repossessed if you do not keep up repayments on your mortgage or loans secured on it.

Best Fit Mortgages LTD Registered office address: 60 Chiltern Road, St. Helens, England, WA9 2HT. Registered in England and Wales No: 15722235

Making a complaint: It is our intention to provide you with a high level of customer service at all times. If there is an occasion when we do not meet these standards and you wish to register a complaint, please write to: Compliance Department; Connect IFA Ltd, 39 Station Lane, Hornchurch, RM12 6JL or call: 01708 676110. If you cannot settle your complaint with us, you may be entitled to refer it to the Financial Ombudsman Service www.financial-ombudsman.org.uk

Best Fit Mortgages LTD is an Appointed Representative of Connect IFA Limited 441505 which is Authorised and Regulated by the Financial Conduct Authority and is entered on the Financial Services Register under reference 1017669. The FCA do not regulate some forms of Business Buy to Let Mortgages and Commercial Mortgages to Limited Companies. A fee will be payable for arranging your mortgage. Your consultant will confirm the amount before you choose to proceed, but this is typically 0.5% of the mortgage balance, e.g. £500 for a mortgage of £100000. The guidance and/or advice contained within this website is subject to the UK regulatory regime and is therefore primarily targeted at consumers based in the UK.

© 2024. All rights reserved.

Commission disclosure: We are a credit broker and not a lender. We have access to an extensive range of lenders. Once we have assessed your needs, we will recommend a lender(s) that provides suitable products to meet your personal circumstances and requirements, though you are not obliged to take our advice or recommendation. Whichever lender we introduce you to, we will typically receive commission from them after completion of the transaction. The amount of commission we receive will normally be a fixed percentage of the amount you borrow from the lender. Commission paid to us may vary in amount depending on the lender and product. The lenders we work with pay commission at different rates. However, the amount of commission that we receive from a lender does not have an effect on the amount that you pay to that lender under your credit agreement.

Not all services we offer are covered by the FCA.